2020 Roth IRA Contribution and Income Limits: Your Go-To Guide

As you may already know, a Roth IRA is a pretty lovely boon for those saving for retirement. It’s an individual retirement account, meaning that you initiate the account and add money to it through your working years rather than your employer. The real sparkle of a Roth IRA is that even though you pay taxes on the money you put in the account, it is allowed to grow (and keep growing), all with the ability to withdraw the funds tax-free if you’ve had the account a minimum of 5 years and are at least 59 1/2 years old. Since these tax savings are so abundant, the IRS has contribution eligibility limits based on income and filing status. It’s important to be aware of your income limits for a Roth IRA.

Let’s take a look at the 2020 Roth IRA limits that you should be aware of as you enter the new year.

What are the Roth IRA Contribution and Income Limits?

You can contribute up to $6,000 to an IRA if you are under the age of 50 in 2020. You can contribute an extra $1,000 if you are over the age of 50, meaning your limit is $7,000.

Make sure to take note that these are the contribution restrictions for your total IRA contributions for the year. If you have both a traditional IRA and a Roth IRA and you are below the age of 50, your contributions to both accounts can’t total more than $6,000. How does all of this work with married couples? A couple is not able to open an IRA. It is an individual retirement account, not a dual account.

If you qualify under the eligibility terms, which we will review now, as a couple, you can each open a Roth IRA and contribute the maximum of $12,000 combined if you’re both under 50, or a total of $14,000 between the two IRAs if you are both over the age of 50.

Income Limits: Do I Earn Too Much for a Roth IRA?

To begin, to contribute to any form of IRA, you must have taxable income from either a job as an employee or salary from self-employment. To see if you qualify, you’ll have to calculate your modified adjusted gross income, sometimes abbreviated as modified AGI or MAGI. That is your gross adjusted income, which you can locate on tax forms 1040, 1040a, or 1040ez-with some deductions such as contributions to health savings accounts or student loan interest payments. We will use the MAGI for our purposes here since this is what matters when looking at eligibility and income limits for a Roth IRA.

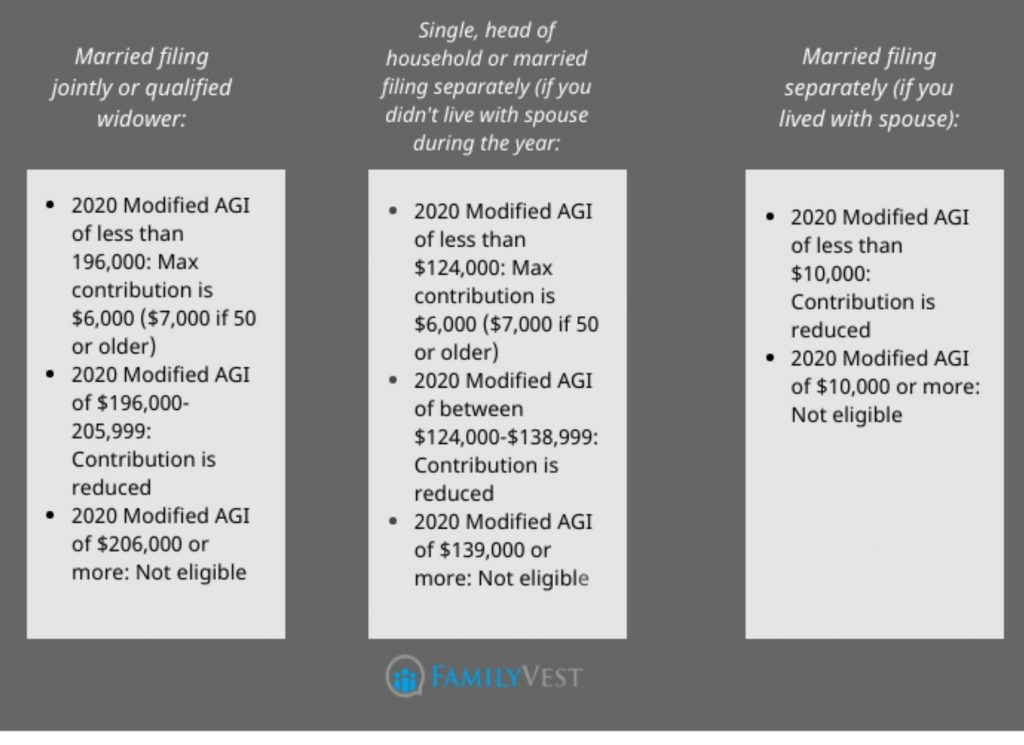

In 2020, if you are single and head of household or married and filing separately (and did not live with your spouse at any point for the tax year), you can contribute:

- If your income is less than $124,000, the maximum amount.

- If your income is at least $124,000, but less than $139,000, an amount that phases out as you earn more.

- If your income is $139,000 or higher, nothing.

If you are married (filing jointly) or a qualifying widower, you are able to contribute:

- If your income is less than $196,000, the maximum amount.

- If your income is at least $196,000 but less than $206,000, an amount that phases out as you earn more.

- If your income is over $206,000, nothing.

If you are married and filing separately (and lived with your spouse at any time during the tax year), you are able to contribute:

- If your income is under $10,000, a reduced amount.

- If your income is $10,000 or higher, nothing.

Is There an Age Limit When Contributing to a Roth IRA?

As long as you have taxable income, you can open a Roth IRA at any age. The perks don’t stop there; you can then continue to contribute to it for the rest of your life if you are still earning income since there is not an age limit for Roth IRAs.

Additionally, you do not have to take mandatory withdrawals, or RMDs, because there are no obligatory minimum distributions. So consequently, a beneficiary can withdraw funds from it tax-free after you are deceased.

All of these benefits are wonderful, but you have to keep in mind that if you decide to withdraw your Roth IRA earning early, that is before age 59 1/2 or before the account is five years old, you will frequently pay taxes plus a 10% penalty to do so. However, you do have the ability to withdraw contributions whenever you like, and you also may be able to dodge sanctions for early withdrawal in certain instances, such as for specific medical expenses or a home purchase.

What if I’m Hitting a Wall with Some of These Limits?

We’ve looked at the Roth IRA limits for 2020, and you may be wondering what you can do for your saving plan if you find yourself ineligible. Here are a couple of tips and alternatives to consider.

1. Add to Your 401(k) Contributions

A 401(k) is funded with your pre-taxed money, unlike a Roth IRA, so it lowers your taxable income. If you earn too much to qualify for a Roth IRA, but you have access to a 401 (k) or some other employer-sponsored plan, you can make additional contributions to your 401 (k) to reduce your taxable income as a possible option.

If you’re under 50 years of age, you can contribute up to $19,500 to a 401(k) in 2020. If you are older than 50, and your plan permits catch-up contributions, the maximum contribution is $26,000.

2. Initiate an IRA for a Spouse That is Not Working

There is an exception to the rule regarding the need for earned income when opening an IRA. If you are married and have a spouse that is not employed, you can open either a traditional or Roth IRA for them at the maximum allowable amount for their age, given that you have income equal to the amount you’re putting into your own IRA and your spouse’s IRA. Remember, You would need to follow the same IRA contribution limits.

The 2020 Roth IRA may seem complicated

For more about Roth IRAs and other informative financial topics, feel free to visit our Farther-FamilyVest blog.

To schedule a consultation with Farther-FamilyVest, contact us today.

Farther-FamilyVest is your local Fiduciary Financial Advisor in Destin and fiduciary financial advisor on 30A!